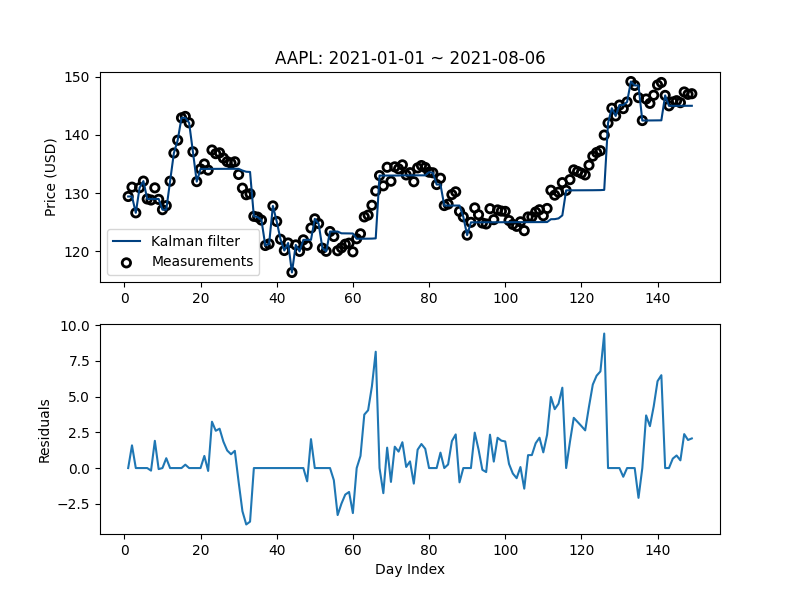

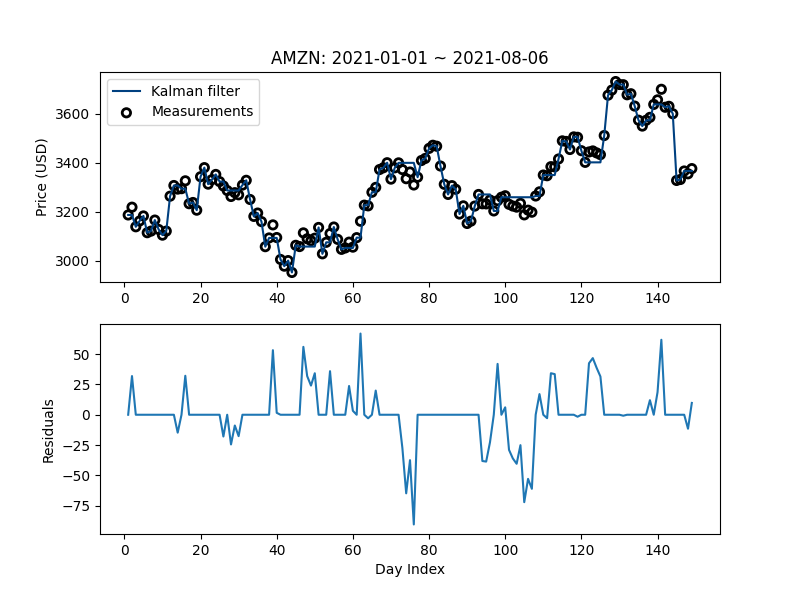

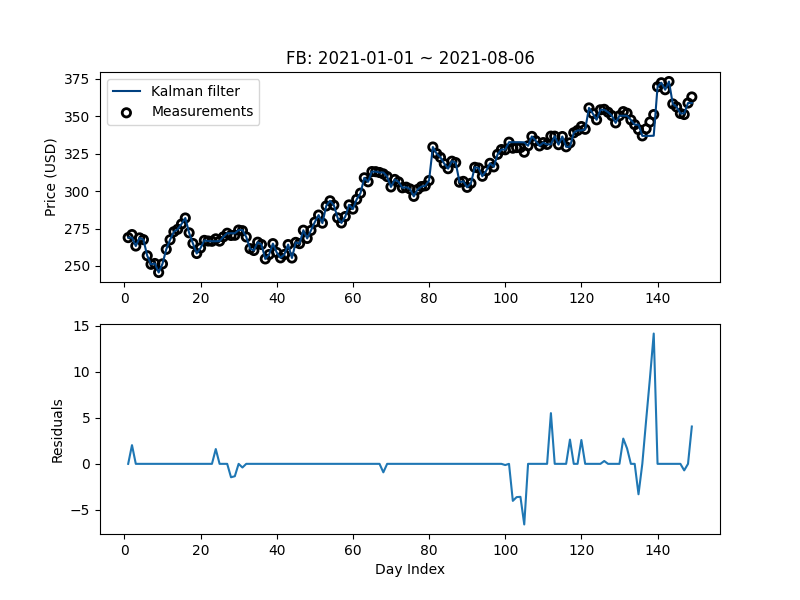

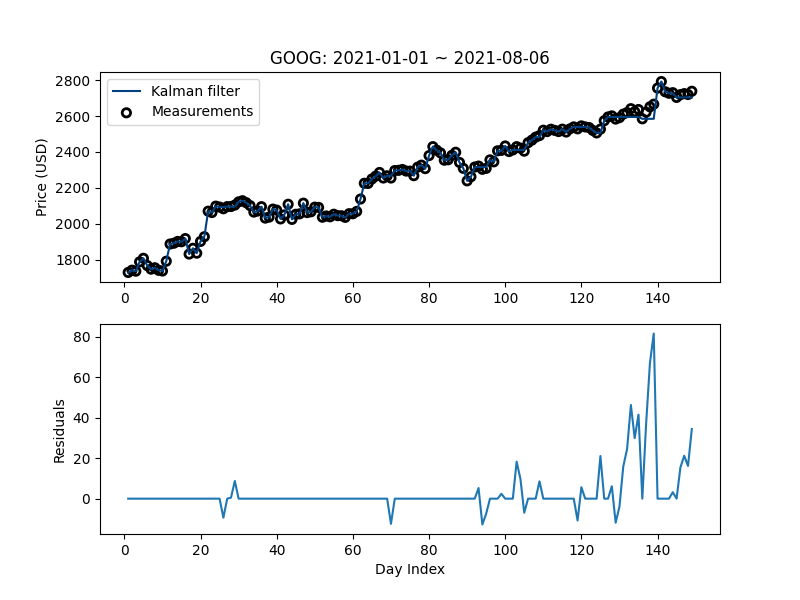

Kalman Filter & the Mean-Reverting Strategy

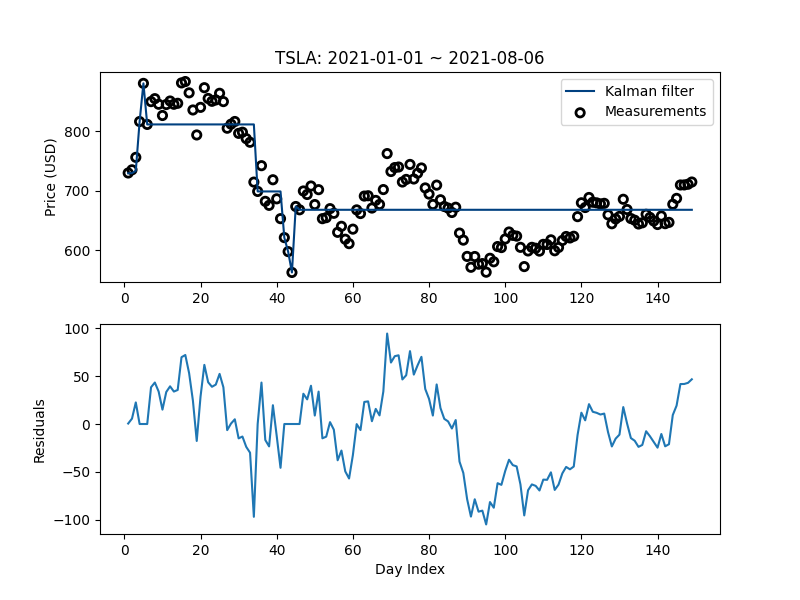

If a stock price series is mean-reverting, we could trade on it and make a profit if we could accurately estimate its means and standard deviations for the near future. Kalman filter is an excellent algorithm for doing that. In this project, we implemented a 1D Kalman Filter in Python to forecast the near-future mean prices of AAPL, AMZN, FB, GOOG, and TSLA stocks based on their daily close price and volume data between January 1 and August 6, 2021. We discovered that only TSLA showed a mean reverting pattern for this period. Our Kalman filter is smart enough to wait and see if a real trend develops before reflecting it in its forecasts. Read our paper to understand how Kalman filter works its magic.